Attorney-Approved Promissory Note Form for Missouri State

Other Missouri Forms

Notice to Quit Missouri - It provides a specified timeframe for the tenant to leave the premises.

Mo Bill of Sale - Using a Bill of Sale can help clarify any misunderstandings about the transaction details.

For those looking to navigate the complexities of firearm transactions, a comprehensive Georgia Firearm Bill of Sale is crucial for ensuring a smooth transfer of ownership. You can familiarize yourself with the form by visiting the complete guide on the Firearm Bill of Sale process.

Clay County Mo Probate Court - Some jurisdictions may allow the affidavit process for certain types of joint property or accounts.

Detailed Steps for Filling Out Missouri Promissory Note

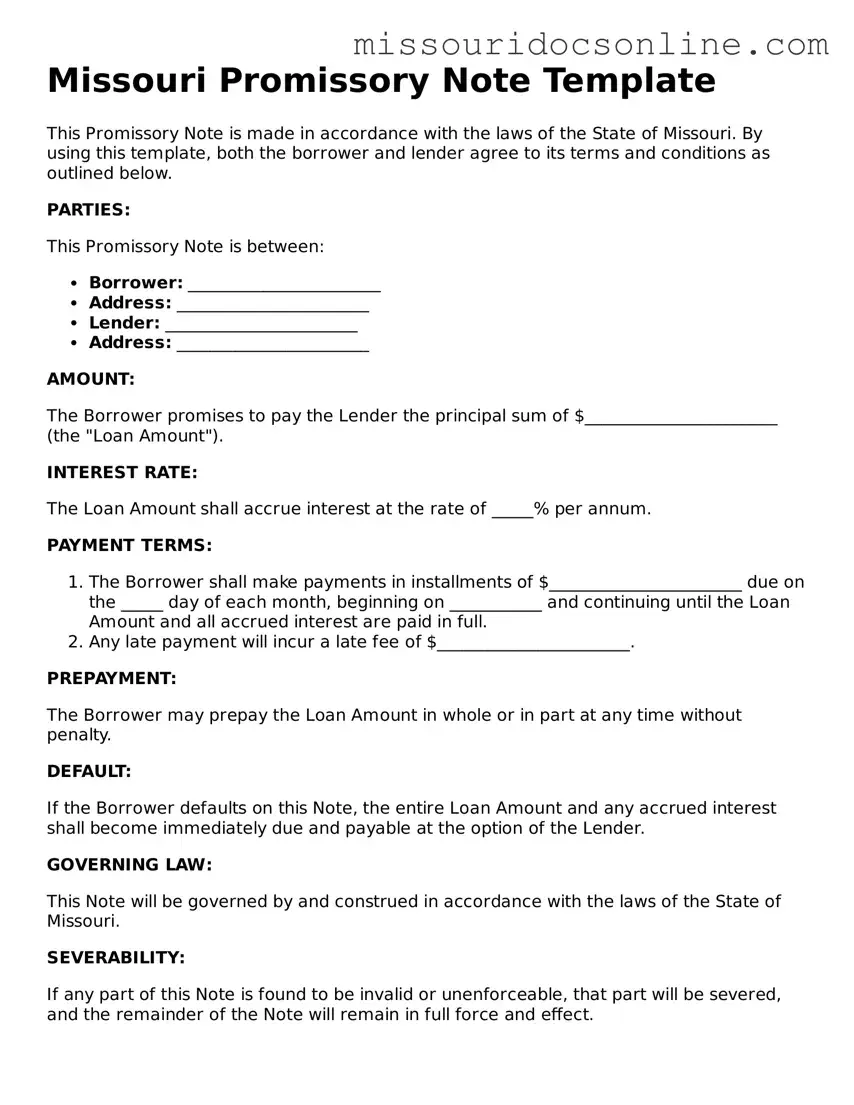

Filling out the Missouri Promissory Note form is an important step in formalizing a loan agreement. Once completed, this document will outline the terms of the loan and establish the obligations of both the borrower and the lender. Follow these steps to ensure that you fill out the form correctly.

- Begin by entering the date at the top of the form. This date marks when the agreement is made.

- Next, provide the name and address of the borrower. This identifies who is responsible for repaying the loan.

- Then, enter the name and address of the lender. This indicates who is providing the loan.

- Specify the principal amount of the loan. This is the total amount borrowed, without any interest included.

- Indicate the interest rate, if applicable. This is the percentage that will be added to the principal amount over time.

- Outline the repayment schedule. Include details about when payments are due and how often they will occur (e.g., monthly, quarterly).

- Include any late fees or penalties for missed payments, if relevant. This helps clarify the consequences of late payments.

- State the maturity date. This is the final date by which the loan must be fully repaid.

- Both the borrower and lender should sign and date the form at the bottom. This signifies that both parties agree to the terms outlined in the note.

After completing the form, make copies for both parties. Keep these copies in a safe place. This ensures that both the borrower and lender have a record of the agreement and can refer to it in the future if necessary.

Misconceptions

Understanding the Missouri Promissory Note form can be challenging due to various misconceptions. Here are five common misunderstandings about this important financial document:

-

All Promissory Notes Are the Same:

Many people believe that all promissory notes are identical in structure and purpose. In reality, each state, including Missouri, has specific requirements that must be met for a promissory note to be legally binding. These requirements can vary significantly, making it essential to use the correct form for your jurisdiction.

-

Promissory Notes Only Apply to Loans:

While promissory notes are commonly associated with loans, they can also be used for other types of financial agreements. For example, they may be utilized in business transactions or personal loans between friends and family. Their versatility makes them a valuable tool in various financial situations.

-

A Notarized Signature Is Always Required:

Some individuals think that a notarized signature is necessary for a promissory note to be valid. However, in Missouri, notarization is not a requirement for a promissory note to be enforceable. As long as the terms are clear and both parties agree, the document can be legally binding without a notary's involvement.

-

Verbal Agreements Are Just as Good:

There is a common belief that verbal agreements can hold the same weight as written promissory notes. While verbal agreements can be legally binding in some situations, they are much harder to enforce. A written promissory note provides clear evidence of the terms and conditions, making it a more reliable option.

-

Once Signed, a Promissory Note Cannot Be Changed:

Many assume that once a promissory note is signed, its terms are set in stone. In fact, parties can negotiate changes to the terms, provided both agree to the modifications. It is advisable to document any changes in writing to avoid misunderstandings in the future.

Dos and Don'ts

When filling out the Missouri Promissory Note form, it is important to follow certain guidelines to ensure accuracy and legality. Here are six things you should and shouldn't do:

- Do read the entire form carefully before starting to fill it out.

- Do provide accurate information regarding the borrower and lender.

- Do specify the repayment terms clearly, including interest rates and due dates.

- Do sign and date the form to make it legally binding.

- Don't leave any sections blank; fill in all required fields.

- Don't use unclear language or abbreviations that may cause confusion.

Similar forms

- Loan Agreement: Similar to a promissory note, a loan agreement outlines the terms and conditions under which a borrower receives funds from a lender. It specifies repayment terms, interest rates, and other obligations.

- Mortgage: A mortgage is a specific type of loan agreement secured by real property. Like a promissory note, it includes repayment terms, but it also involves collateral in the form of the property itself.

- Installment Agreement: This document allows a borrower to repay a debt in scheduled payments over time. It shares the structure of a promissory note by detailing the payment schedule and interest rate.

- Secured Note: A secured note is similar to a promissory note but includes collateral to back the loan. This adds an extra layer of security for the lender.

- Unsecured Note: Unlike a secured note, an unsecured note does not have collateral backing it. It functions like a promissory note, outlining the borrower's promise to repay without any security interest.

- Personal Loan Agreement: This document details the terms of a personal loan between individuals. It includes repayment terms and conditions, similar to a promissory note.

- Credit Agreement: A credit agreement establishes the terms under which a borrower can access credit. It includes repayment terms and interest rates, akin to a promissory note.

- Business Loan Agreement: This agreement outlines the terms of a loan for business purposes. It specifies repayment schedules and obligations, similar to a promissory note.

- Motor Vehicle Bill of Sale: This document is crucial for the sale of a vehicle, providing essential details such as the buyer and seller's information, vehicle specifics, and sale price. For more information, you can visit TopTemplates.info.

- Debt Settlement Agreement: This document outlines the terms under which a borrower agrees to pay a reduced amount to settle a debt. It includes repayment terms, resembling a promissory note.

- Forbearance Agreement: A forbearance agreement allows a borrower to temporarily reduce or suspend payments. It includes specific terms for repayment, similar to a promissory note.

File Specs

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a certain time. |

| Governing Law | The Missouri Uniform Commercial Code governs promissory notes in Missouri, specifically under Chapter 400. |

| Parties Involved | Typically, there are two main parties: the maker (the person promising to pay) and the payee (the person receiving the payment). |

| Key Components | A valid promissory note includes the principal amount, interest rate, payment terms, and signatures of the parties involved. |

| Interest Rates | Missouri allows parties to agree on an interest rate, but it must comply with state usury laws to avoid excessive charges. |

| Enforceability | For a promissory note to be enforceable, it must be clear, unambiguous, and signed by the maker. |

| Default Consequences | If the maker defaults, the payee has the right to pursue legal action to recover the owed amount. |

| Transferability | Promissory notes can often be transferred to another party, allowing the new holder to enforce the note. |

| Notarization | While notarization is not required, having the document notarized can provide an extra layer of verification and security. |