Blank Missouri 4795 Form

Consider Common PDFs

Do You Get Money Back for Turning in License Plates - Incorrectly filled forms may delay processing of the request.

In Georgia, ensuring a smooth transaction when buying or selling a vehicle is crucial, and the use of a proper Bill of Sale is essential for legal clarity. By utilizing the Georgia Motor Vehicle Bill of Sale form, parties can effectively document the sale, which includes necessary details such as the vehicle's make, model, year, VIN, and sale price, along with the signatures of both the seller and buyer. For more comprehensive templates and guidance on creating this important document, visit TopTemplates.info, which offers valuable resources for ensuring a secure and legally binding transaction.

Mo Division of Employment Security - Mail the original form to the designated address in Jefferson City, MO.

Detailed Steps for Filling Out Missouri 4795

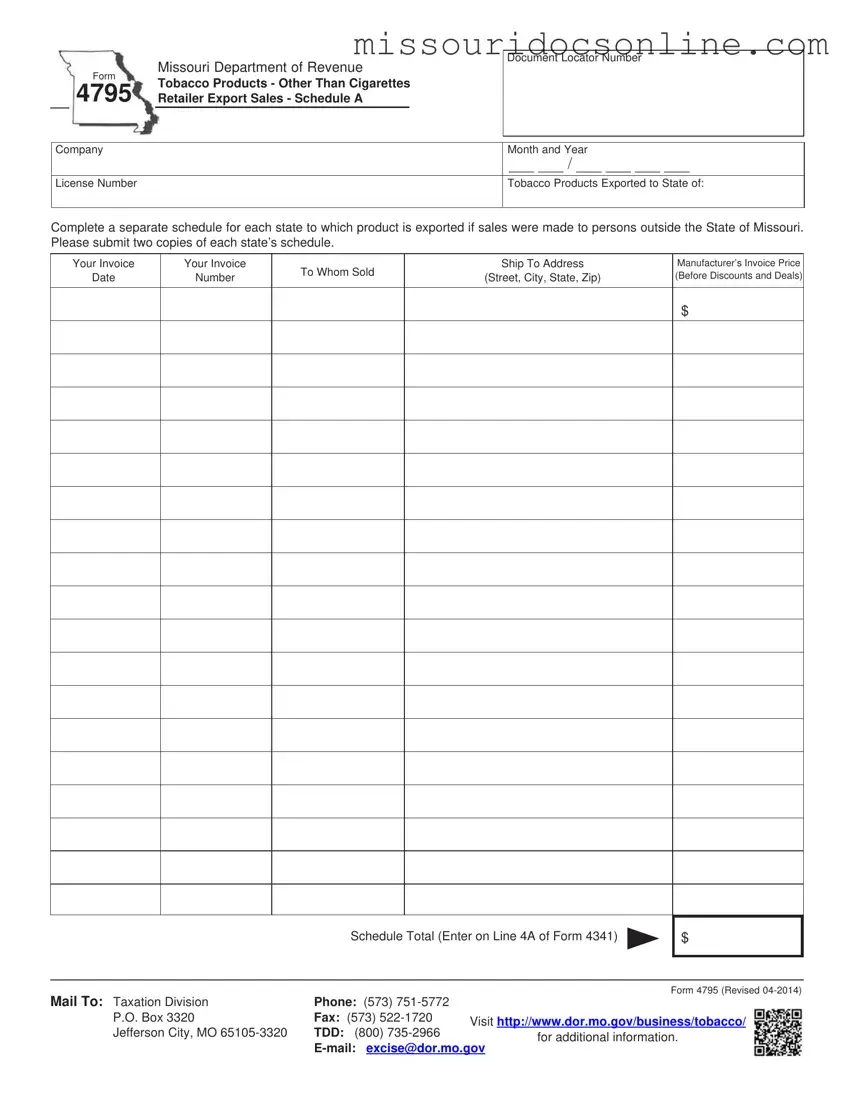

Filling out the Missouri 4795 form requires careful attention to detail. This form is used for reporting tobacco product exports, and accuracy is essential to ensure compliance with state regulations. Below are the steps to guide you through the process of completing the form.

- Obtain the Missouri 4795 form. You can find it on the Missouri Department of Revenue website or request a copy from their office.

- At the top of the form, enter the Document Locator Number as "4795".

- Fill in your Company License Number in the designated space.

- Indicate the Month and Year for which you are reporting. Use the format MM/YYYY.

- Specify the State to which the tobacco products are exported. If you have sales to multiple states, complete a separate schedule for each state.

- For each sale, enter the Invoice Date and the Invoice Number in the appropriate fields.

- Fill in the To Whom Sold section with the name of the buyer.

- Provide the Ship To Address, including the street, city, state, and zip code.

- Enter the Manufacturer’s Invoice Price before any discounts or deals. Make sure to include the dollar amount.

- Calculate the Schedule Total and enter this amount on Line 4A of Form 4341.

- Once completed, make two copies of the schedule for each state you reported. Keep one for your records and submit the other as required.

- Mail the completed form and any required schedules to the Taxation Division at the address provided on the form.

After filling out the form, ensure that all information is accurate and complete before submission. This will help avoid any potential issues with your report. If you have questions or need assistance, consider reaching out to the Taxation Division using the contact information provided on the form.

Misconceptions

- Misconception 1: The Missouri 4795 form is only for cigarette sales.

- Misconception 2: Only one schedule is needed for all exported tobacco products.

- Misconception 3: The invoice date and number are optional fields.

- Misconception 4: Submitting the form electronically is not allowed.

- Misconception 5: There is no need to keep copies of the submitted schedules.

- Misconception 6: The form can be submitted at any time without a deadline.

This form is specifically designed for reporting tobacco products other than cigarettes. Retailers must use it for all types of tobacco exports.

Each state to which tobacco products are exported requires a separate schedule. This ensures accurate reporting for each jurisdiction.

Both the invoice date and invoice number are mandatory. These details help verify the transactions and maintain accurate records.

While the form must be mailed, there are options for electronic communication with the Taxation Division for inquiries and additional information.

Retailers should retain copies of all submitted schedules for their records. This practice aids in future audits and compliance checks.

There are specific deadlines for submitting the Missouri 4795 form. Retailers must be aware of these timelines to avoid penalties.

Dos and Don'ts

When filling out the Missouri 4795 form, keep the following tips in mind to ensure accuracy and compliance.

- Do double-check your company license number for accuracy.

- Don't leave any required fields blank; fill in all necessary information.

- Do complete a separate schedule for each state if you exported to multiple states.

- Don't forget to submit two copies of each state's schedule.

- Do ensure that the invoice date and number are clearly indicated.

- Don't use abbreviations for the ship-to address; provide the full address.

- Do enter the manufacturer's invoice price before any discounts.

Following these guidelines will help in properly completing the form and avoiding potential issues.

Similar forms

The Missouri 4795 form is primarily used for reporting tobacco product exports by retailers. Several other documents serve similar purposes in various contexts. Here’s a list of seven documents that share similarities with the Missouri 4795 form:

- Form 4341: This form is related to the reporting of tobacco products and is used to summarize the tax due on tobacco sales. Like the Missouri 4795, it requires detailed information about sales and exports.

- Form 5000: Used for reporting sales of alcohol products, this form collects data on exports and sales similar to how the Missouri 4795 does for tobacco products.

- Form 1065: This is a partnership tax return form. It requires reporting income, deductions, and credits, similar to how the Missouri 4795 requires detailed sales information.

- Form 941: This form is used for reporting payroll taxes. It includes information about employee wages and tax withholdings, paralleling the detailed reporting aspect of the Missouri 4795.

- Form 1099: Issued for reporting various types of income, this form shares the need for detailed information about transactions, much like the Missouri 4795 does for tobacco exports.

- Form W-2: This form reports wages paid to employees and the taxes withheld. It requires precise information about earnings, similar to the detailed invoice requirements of the Missouri 4795.

- California Self-Proving Affidavit Form: To streamline your estate planning, utilize our essential Self-Proving Affidavit form to ensure your will is validated efficiently.

- Form 720: This form is used for reporting excise taxes on certain goods, including tobacco. Like the Missouri 4795, it requires information on sales and exports for tax purposes.

Document Information

| Fact Name | Description |

|---|---|

| Purpose | The Missouri 4795 form is used for reporting tobacco products exported to states outside of Missouri. |

| Governing Law | This form is governed by Missouri Revised Statutes, specifically Chapter 149 regarding tobacco taxation. |

| Submission Requirements | Two copies of each state’s schedule must be submitted if sales are made to persons outside Missouri. |

| Contact Information | For questions, individuals can contact the Taxation Division at (573) 751-5772 or via email at excise@dor.mo.gov. |